Between the skyrocketing cost of living and the general weight of economic uncertainty, most homeowners I talk to are just trying to keep their heads above water. But as soon as we bring up the idea of a refinance, the vibe shifts. Usually, it’s met with defensive: “I’ve worked too hard to pay this down” or “I don’t want to start my 25 or 30 years all over again.”

I get it. It feels like you’re undoing years of hard work. But if we’re being honest? A lot of that resistance isn’t based on ego. We’ve been conditioned to think that “paying down the mortgage” is the metric of success, even when the rest of the ship is taking on water.

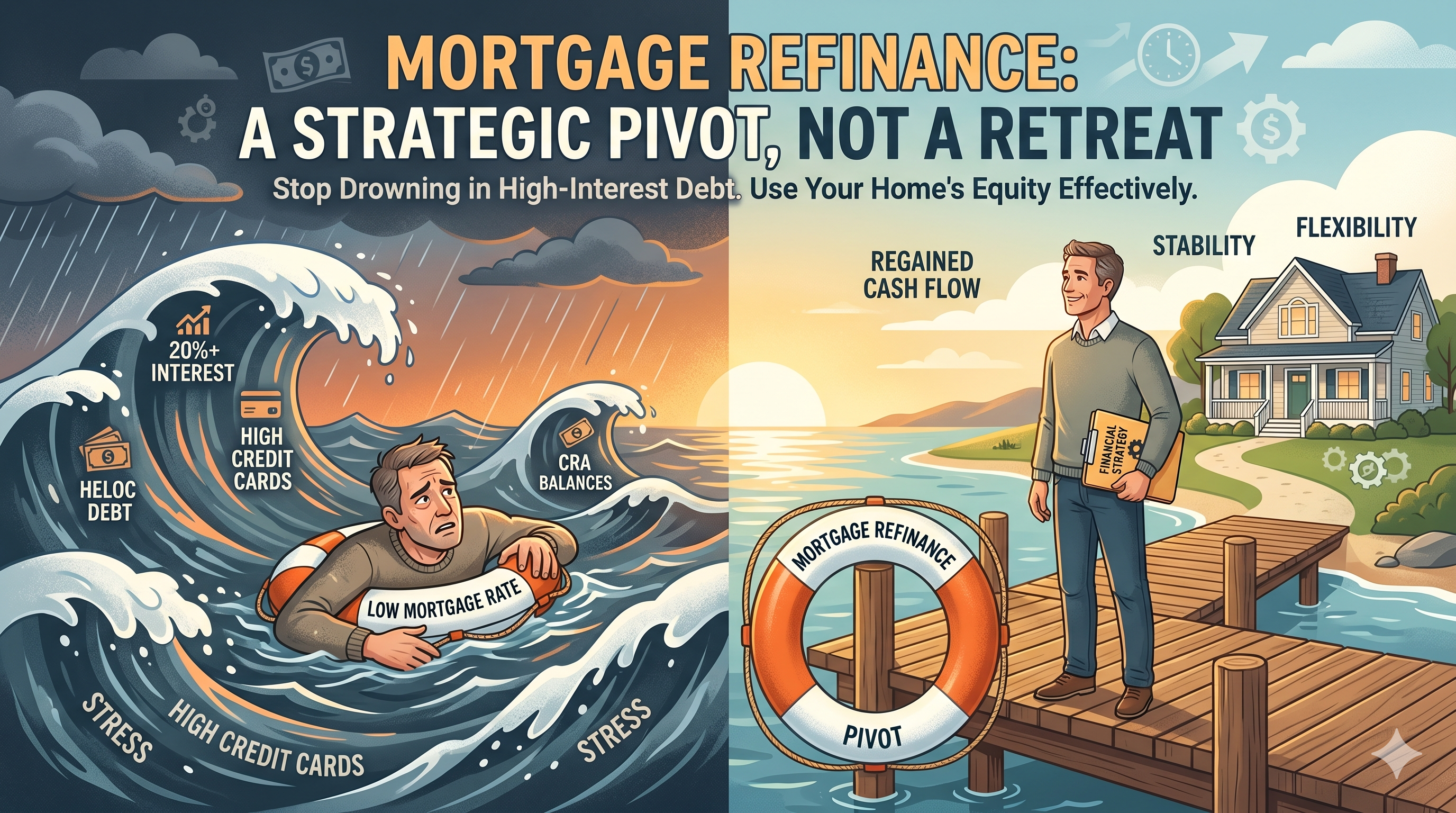

The Danger of Rate Tunnel Vision

We need to talk about the rate tunnel vision. I see it every week: a homeowner clinging to a “great” mortgage rate like a life raft, while they are drowning in high-interest credit cards, CRA balances, or unsecured loans.

When you’re paying 20%+ on consumer debt, that “low” mortgage rate becomes a vanity metric. It’s not saving you money if it’s preventing you from:

- Building a real retirement nest egg.

- Funding post-secondary education.

- Enjoying your life instead of “surviving” the month.

At some point, we have to stop looking at the mortgage in isolation and start looking at the total cost of your life.

Hard Questions To Consider

If you’re feeling the squeeze, it’s time to audit your reality:

- Does your stomach knot up when the 1st of the month approaches?

- Are you building equity, or are you “robbing Peter to pay Paul” by dipping into savings to cover monthly bills?

- Credit Cards used cover when you have overspent that month?

- Personal or HELOC, cover the surprises or just the necessities?

- What is the “interest” on your stress levels and your family’s future?

Think Of Refinancing as a pivot, not a retreat.

A mortgage isn’t a debt to be conquered it’s the most powerful financial tool you own. When we stop viewing a refinance as “going backwards,” we can start viewing it as a pivot. I’ve helped clients use their equity to:

- Reclaim their cash flow and finally breathe again,

- Bridge the gap during career shifts or business lulls,

- Protect their future by clearing debt that was eating their retirement contributions,

- Stabilize during high-stress transitions like a divorce,

The mortgage industry is obsessed with “the lowest rate,” but it is a race to the bottom that ignores the big picture. We should be talking about financial positioning. A great strategy it’s about flexibility and risk management. Can your mortgage handle a “life happens” moment? Is it working for you, or are you working for it?

Restructuring your debt isn’t a sign of failure it’s a chess move. It’s about taking the equity you’ve built and putting it to work where it’s needed most right now.

I’d love to hear your take: Is the ego of “starting over” keeping people trapped in high-stress financial situations? Or is there still a stigma that a “reset” is a bad thing?